This post may contain affiliate links, which means if you enroll through my link, I’ll receive a small commission at no extra cost to you.

Healthcare savings just got a major upgrade. On July 4, 2025, the One Big Beautiful Bill Act (H.R.1) was signed into law, expanding several tax-advantaged health benefits.

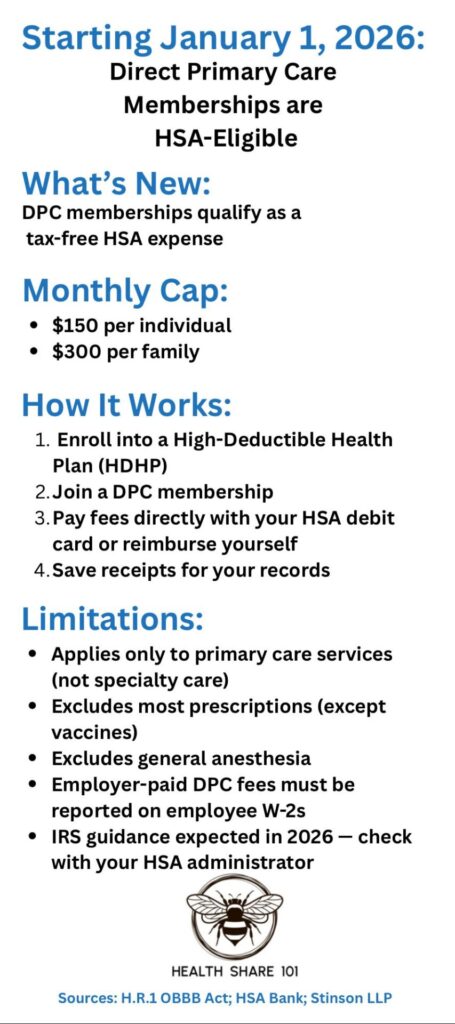

One of the biggest changes? Starting January 1, 2026, Direct Primary Care (DPC) memberships will finally be HSA-eligible.

That means Americans can now use tax-free HSA funds to pay for their monthly DPC membership — a change that removes a long-standing barrier and makes healthcare both simpler and more affordable.

In this post, I’ll walk you through:

- Why DPCs weren’t HSA-eligible before

- What’s changing in 2026

- How to use HSA funds for DPC memberships

- Limits and restrictions you need to know

- Why this matters for families, small business owners, and the self-employed

Why DPCs Weren’t HSA-Eligible Before

Direct Primary Care is a membership model where you pay your doctor directly for unlimited primary care visits. It’s not insurance, but a simple way to access routine and preventive care without surprise bills.

The IRS, however, historically classified DPC memberships as a form of “other coverage.”

Under the old rules:

- You could still contribute to your HSA if you had a qualified High-Deductible Health Plan (HDHP).

- But you could not use your HSA funds to pay DPC membership fees, since they weren’t considered a qualified medical expense.

This left patients in a frustrating spot: either pay for DPC out-of-pocket with after-tax dollars, or miss out on the tax advantages of their HSA.

DPCs Become HSA-Eligible in 2026

That restriction is finally gone. Starting January 1, 2026:

- ✅ DPC memberships are now HSA-compatible

- ✅ Membership fees are considered qualified medical expenses

- ✅ You can pay with your HSA debit card or reimburse yourself

- ✅ Monthly cap: $150 individual / $300 family

This breakthrough combines the best of both worlds: predictable primary care and tax-advantaged savings.

How to Use HSA Funds for Your DPC Membership

Here’s how it will work in practice:

- Keep your HDHP. You’ll still need a high-deductible health plan to stay HSA-eligible.

- Join a DPC membership. Just keep in mind that you can only reimburse up to $150 per month for individuals or $300 per month for families from your HSA.

- Pay directly with your HSA. Use your HSA debit card for your monthly fee, or reimburse yourself after paying out of pocket.

- Save receipts. As with all HSA expenses, keep documentation in case the IRS ever asks.

Bronze & Catastrophic ACA Plans Are Now HSA-Eligible Too

There’s another important update in the new law that goes hand-in-hand with the DPC change.

Starting January 1, 2026, any Bronze or Catastrophic plan purchased through the ACA Marketplace will automatically be treated as an HSA-qualified High-Deductible Health Plan (HDHP).

This is a big deal because in the past, only certain HDHPs met the IRS rules for HSA eligibility. Many Bronze and Catastrophic plans didn’t qualify. With the new law:

- ✅ Individuals with Bronze or Catastrophic plans can now open and contribute to an HSA.

- ✅ These plans are officially recognized as HDHPs for HSA purposes.

- ✅ This means more Americans will have access to tax-advantaged savings while using lower-premium ACA plans.

For patients who want to pair a low-cost ACA plan with a Direct Primary Care membership, this update makes that possible — and more affordable — starting in 2026.

Limits of Using HSA Funds for DPC

While this is a huge win, there are a few restrictions:

- Applies only to primary care services (not specialty care)

- Excludes most prescriptions (except vaccines)

- Excludes general anesthesia and other advanced services

- Employers who pay DPC fees on your behalf must report those contributions on your W-2

- Final IRS guidance will clarify details, so always check with your HSA administrator in 2026

Why This Matters for Families and the Self-Employed

This change removes one of the biggest barriers to combining two of the most consumer-friendly healthcare options: HSAs and DPC.

For example:

- A family paying $250/month for a DPC membership could save $900/year in taxes by using HSA funds (assuming a 30% tax bracket).

- Small business owners and freelancers, who often juggle unpredictable healthcare costs, gain a way to simplify primary care while still saving for larger medical needs.

This isn’t just a policy tweak — it’s a fundamental shift toward affordable, personalized, tax-smart healthcare.

Can You Use a Health Share With an HSA?

This is one of the most common questions I get, so let’s clear it up.

Health shares are not considered High-Deductible Health Plans (HDHPs).

An HDHP is a specific type of insurance plan defined by the IRS with certain minimum deductibles and maximum out-of-pocket limits. Since health shares are not insurance, they don’t meet that definition.

That means:

- Having a health share alone does not make you eligible to contribute to a Health Savings Account (HSA).

- To open and contribute to an HSA, you must be enrolled in a qualified HDHP.

However, some people combine the two:

- The HDHP makes you HSA-eligible

- The HSA gives you tax advantages and can pay for things like DPC memberships (starting 2026)

- The health share helps with larger medical needs, usually at a lower monthly cost than traditional insurance

⚠️ One important note: Not all expenses a health share may help with are considered “qualified medical expenses” under IRS rules. Your health share might help with a bill, but that doesn’t automatically mean you can also run that expense through your HSA.

Bottom line:

A health share alone won’t qualify you for an HSA, but you can layer a health share on top of an HDHP if you want both.

What This Means for You

Starting in 2026, you don’t have to choose between a Health Savings Account and Direct Primary Care. You can finally have both.

If you’ve been on the fence about joining a DPC practice or opening an HSA, now’s the time to start planning. Pairing these tools could save your family hundreds — even thousands — each year, while giving you more control over your healthcare.

Want to share this Infographic?

Feel free to use it on your website — just make sure to include attribution back to HealthShare101.com.

Copy the code:

Next, just paste thie code into a Custom HTML block on your website to display the infographic on your website!

Health shares are not insurance and do not offer insurance coverage. Membership in a health share does not guarantee the payment or reimbursement of medical expenses. Each organization operates under its own membership guidelines, which determine what expenses may be eligible for sharing. This publication is for informational purposes only and is not provided by an insurance company. For state-specific notices and full program details, please visit the respective health share’s official website.

vs Zion HealthShare")

")

Leave a Reply