This post may contain affiliate links, which means if you enroll through my link, I’ll receive a small commission at no extra cost to you.

A lot of people are looking into health shares right now… and for good reason. Traditional health insurance has gotten expensive, and many families are looking for options that feel more affordable each month.

And lately, I’ve also had a lot of people ask me about CrowdHealth. So if you’ve been comparing CrowdHealth to health shares, this post will clear up the confusion.

Because here’s the most important thing to understand upfront: CrowdHealth is not a health share.

It can look similar from the outside, but the structure is different. And structure matters when you have a real medical bill.

What is CrowdHealth?

CrowdHealth is a monthly membership that uses a crowdfunding-style model to help members with eligible medical bills.

It is not insurance.

And it is not a health share.

In this post, I’ll break down what’s similar between CrowdHealth and health shares, what people often misunderstand, and the three biggest differences that matter most.

CrowdHealth vs health shares: what’s similar

Even though they are not the same, there are a few real similarities.

1) You’re self-pay

With both options, you’re considered a self-pay patient. That’s because neither CrowdHealth or a health share is insurance. So yup, you are “uninsured” with both options.

2) You need to be fairly healthy to join

With either option, symptomatic conditions (diagnosed or not) often come with limitations and waiting periods when you first join. Because pre-existing conditions aren’t included right away (or ever), it means both groups are generally healthier and are spending less on major healthcare costs.

3) You can join year-round

There’s no open enrollment window like there is with traditional health insurance. These memberships are month-to-month, and you can join (or cancel) at any time.

Quick comparison table

Here’s the “big picture” before we go deeper.

| Topic | CrowdHealth | Health shares (varies by program) |

|---|---|---|

| Type | Membership (not insurance) | Membership (not insurance) |

| What it is | Crowdfunding-style model | Community sharing model |

| Monthly structure | Company fee + funding amount | Monthly contribution |

| Large-bill approach | Month-to-month flow | Build a shared-needs fund over time |

| Pricing rules | Often emphasizes “fair market” rates | Some require fair pricing; others don’t (check guidelines) |

Common misunderstandings I hear all the time

When people compare CrowdHealth and health shares, these assumptions come up constantly.

Misunderstanding #1: “CrowdHealth is the only alternative with no religious requirement.”

Not true.

While many health shares are faith-based, there are secular options too, including Sedera, Zion HealthShare, KnewHealth, ShareWELL, ClearShare, and Impact Health Sharing.

So if you don’t want a faith-based program, you still have options.

Misunderstanding #2: “CrowdHealth is the only one with no caps or limits.”

Also not true.

Some health shares, including Christian Healthcare Ministries (Gold plan with CHM Plus), Sedera, Zion HealthShare, and ShareWELL (just to list a few) promote no annual or lifetime limits on eligible sharing requests.

Always verify this in current guidelines, but the point is simple: CrowdHealth isn’t the only place people look for that feature.

Misunderstanding #3: “Health shares make you pay huge medical bills upfront.”

I don’t know a single reputable health share that expects you to show up with a massive check for a large procedure.

In most health shares, you pay your member responsibility amount (whatever you agreed to when you joined) toward the bill. Then, after approval, the rest is handled according to the member guidelines.

The 3 biggest differences (this is where it gets real)

Difference #1: Month-to-month crowdfunding vs pooled member-contribution model

This is the structural difference most people miss.

CrowdHealth operates on a month-to-month basis. Health share communities typically operate with a pool of member contributions that’s collected and managed according to their guidelines.

CrowdHealth’s approach is more like:

- Medical bills come in

- The crowd funds them

- Monthly funding amounts can vary based on what the community needs (within the maximum you agreed to)

With health shares, members send a set monthly contribution that helps build up a pool of member contributions over time. That pool of member contributions can be used to help with eligible large medical bills as they come up, according to the member guidelines.

Bottom line: both models can help with large medical bills, but they are designed differently. That difference affects stability and risk.

Difference #2: CrowdHealth’s per-person advocacy fee (the detail most people miss)

This is the part I really want people to notice before they join.

CrowdHealth’s monthly cost is split into two parts:

- A monthly advocacy fee paid to CrowdHealth as a company

- A monthly funding amount used for members’ eligible medical bills

The current advocacy fee (January 2026) is $60 per person, per month.

When CrowdHealth launched in 2021, the advocacy fee was just $25.

That’s a 140% increase in a few years.

And because it’s per person, families feel the increase the most.

What that looks like in real numbers

Here are the examples I used:

- Individual: $140 maximum monthly funding amount + $60 advocacy fee = $200 total

- $60 out of $200 = 30% going to the company fee

- Family of five: $420 maximum monthly funding amount + $300 advocacy fee = $720 total

- $300 out of $720 = 41% going to the company fee

- Family of eight: $420 maximum monthly funding amount + $480 advocacy fee = $900 total

- $480 out of $900 = 53% going to the company fee

Why this matters

A lot of people only look at the total monthly number.

They don’t realize how much of that total is a fixed per-person company fee.

For context, under the Affordable Care Act, health insurance companies generally have to spend at least 80% of premium dollars on medical care and quality improvement (and 85% in some large-group cases), leaving the remainder for administration, overhead, marketing, and profit.

CrowdHealth isn’t insurance, so those rules don’t apply.

That doesn’t automatically make it “bad.” It just means you should understand the structure before you sign up.

But it’s surprising that an “anti-insurance” company is taking in more for themselves (percentage-wise) than health insurance companies do.

For comparison, health shares will use 90% of funds for funding medical bills and only 10% towards administration costs. With many non-profit health shares, the goal is that the large majority of monthly contributions go toward members’ eligible medical bills, with a smaller portion used for administration. The exact percentage varies by program, so you still need to verify it.

Difference #3: CrowdHealth “fair market” pricing rules

CrowdHealth emphasizes paying a “fair” or “reasonable” market rate.

Here’s the question I always ask:

What decides what “fair” is?

A procedure in New York City won’t price the same as the same procedure in Nebraska. Even within the same state, pricing can swing wildly.

This becomes a real issue when a program says:

- “We’ll only fund up to what we consider fair.”

- “If your local estimate is higher, you’ll need to find another option.”

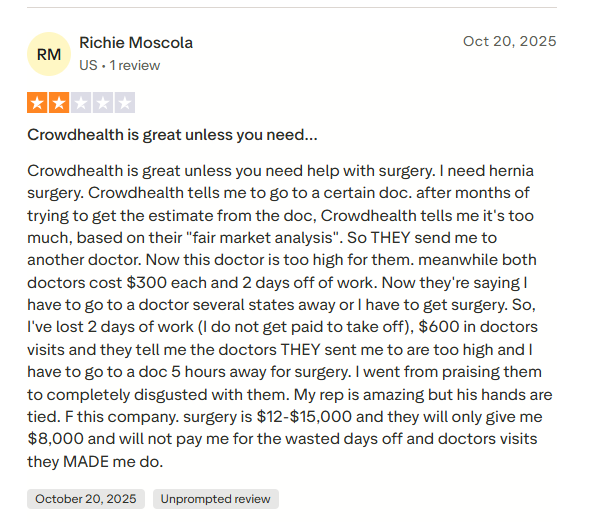

In my video, I shared a member experience where someone said they were routed to multiple doctors because the estimates were considered too high under “fair market” pricing. The member described delays, extra visits, missed work, and being pressured to travel farther for surgery.

CrowdHealth reportedly responded and said some costs would be applied toward the total. Even so, the bigger point remains:

When a program decides a local price isn’t “fair,” it can create stress and uncertainty for the member.

And I don’t know about you, but I don’t want to travel five hours for a surgery when I can just get it locally.

Do health shares do this too?

Some health shares do.

For example, Liberty HealthShare and Medi-Share can use “reasonable and customary” style language, where costs above what they consider reasonable may become the member’s responsibility.

Other programs, including Christian Healthcare Ministries and Zion HealthShare, do not use that same type of “fair market” requirement in the same way. Members often negotiate self-pay pricing (usually by just asking for the cash price), request an itemized bill, and submit it. If the expense is eligible under the member guidelines, it can be shared.

This is why I say this all the time: Marketing is not the same thing as guidelines. Always read the current guidelines before you join.

My concerns with CrowdHealth (and why I still prefer a non-profit health share)

I understand why people are drawn to CrowdHealth. But I personally see a few concerns I can’t ignore.

1) The per-person advocacy fee

It’s a big percentage of the total monthly amount for many households.

And it has increased significantly since launch.

Will it level off? Will it continue to climb? I don’t know. But it’s something you should notice before you join.

2) “Fair market” pricing can become a real problem depending on where you live

If a program decides your local cost isn’t “fair,” it can create delays and push members toward options that aren’t convenient.

Maybe this policy gets more relaxed as time goes on. Maybe not. Either way, it’s a real consideration.

3) Month-to-month structure adds risk

CrowdHealth operates month-to-month. Health shares build up a pool of funds each month, which helps them prepare for larger sharing requests when they come.

I can’t predict the future, but I do know this: healthcare changes fast. Membership models that rely on smooth month-to-month flow can feel more fragile during shocks.

That doesn’t mean CrowdHealth can’t work. It clearly works for many members.

I’m just sharing why I personally prefer a non-profit health share model.

A simple checklist before you join anything

Whether you’re considering CrowdHealth or a health share, here’s what I recommend you check first:

- What are the monthly fees, and which portion goes to the company vs member medical bills?

- Is there a per-person fee? If yes, how does it affect families?

- Does the program use “fair market” or “reasonable and customary” pricing rules?

- How does the program handle large medical bills step-by-step?

- What limitations and waiting periods apply when you first join?

- Can you choose your providers, or will you be routed?

- What do the member guidelines say in plain language?

CrowdHealth FAQ

Is CrowdHealth a health share?

No. CrowdHealth is not a health share. It’s a membership that uses a crowdfunding-style model to help members with eligible medical bills.

Is CrowdHealth insurance?

No. CrowdHealth is not insurance.

What is the CrowdHealth advocacy fee?

CrowdHealth charges a per-person monthly advocacy fee paid to the company, separate from the monthly funding amount used for members’ eligible medical bills.

Does CrowdHealth use “fair market” pricing?

CrowdHealth emphasizes “fair” or “reasonable” market rates. How that applies can depend on the situation and the estimates involved.

Do health shares have fair pricing rules too?

Some do. Others do not. Always verify the current member guidelines for any program you’re considering.

Final thoughts

For the right person, both CrowdHealth and a health share can be a solid alternative to traditional health insurance.

But they are not the same.

If you remember nothing else from this post, remember this: Structure matters more than slogans.

And if you’re new to health shares, I have a free guide that explains how they work and what to look for before joining: Download my free Health Share Guide

Health shares are not insurance and do not offer insurance coverage. Membership in a health share does not guarantee the payment or reimbursement of medical expenses. Each organization operates under its own membership guidelines, which determine what expenses may be eligible for sharing. This publication is for informational purposes only and is not provided by an insurance company. For state-specific notices and full program details, please visit the respective health share’s official website.

vs Zion HealthShare")

Leave a Reply