This post may contain affiliate links, which means if you enroll through my link, I’ll receive a small commission at no extra cost to you.

If you’re self-employed, under 65, and paying for your own healthcare—without any serious pre-existing conditions—you’re not alone. In fact, you’re part of a 30 million–strong group of Americans looking for smart alternatives to traditional health insurance.

Health insurance premiums keep rising. Networks are more limited. And if you don’t get benefits through an employer, it can feel like you’re stuck.

But there’s a growing alternative that’s helping the self-employed get the protection they need without the insurance headaches: health share memberships.

Let’s take a look at the big picture:

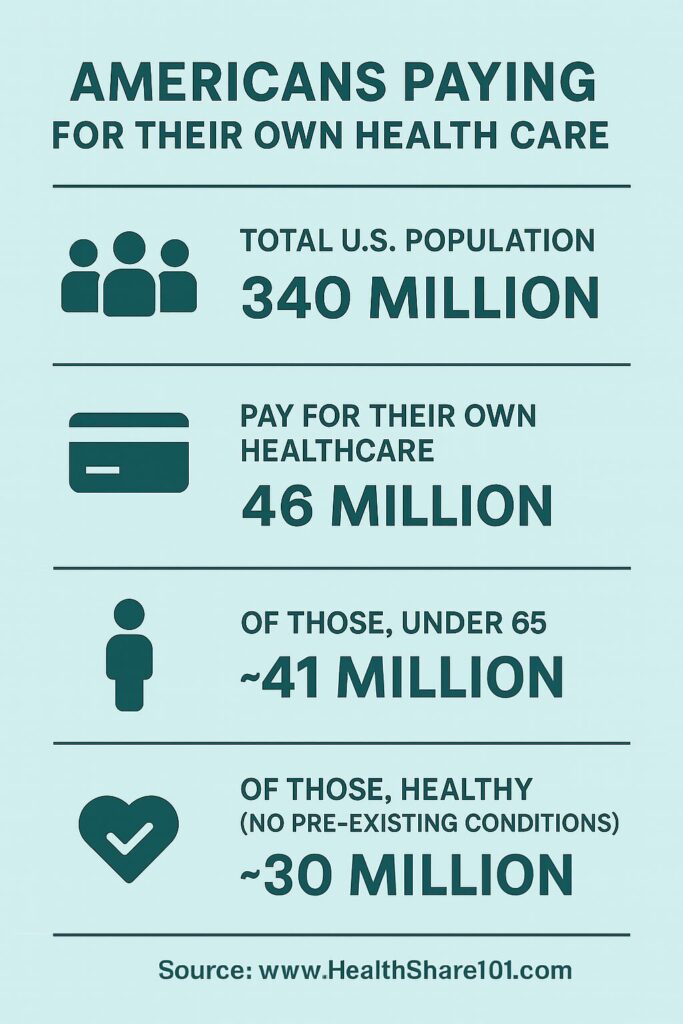

- Total U.S. Population: 340 million

- People who pay for their own healthcare: 46 million

- Of those, under 65: ~41 million

- Of those, healthy (no pre-existing conditions): ~30 million

If you’re self-employed and fit that description—this article is for you.

Why So Many Self-Employed Americans Are Paying for Healthcare Out of Pocket

More and more people are responsible for their own healthcare costs, especially those who:

- Are self-employed or freelance

- Run a small business

- Don’t receive benefits through an employer

- Work in industries without group plans

- Are priced out of ACA plans or don’t qualify for subsidies

In fact, according to recent data, self-employed individuals are twice as likely to shop for alternatives to traditional insurance due to high monthly costs and lack of flexibility. For many, even basic plans with limited access to care can exceed $1,000/month.

That means millions of people are actively searching for more affordable, flexible ways to protect themselves—and that’s where health share memberships come in.

What Is a Health Share Membership?

Health shares are nonprofit, community-based memberships where people contribute monthly to help with each other’s large and unexpected medical expenses.

They are not health insurance, but they can help meet your needs in a similar way—especially for big, unexpected medical events.

What you can expect from most health shares:

- Monthly contributions often 30–50% less than insurance premiums

- No network restrictions—you choose any doctor, hospital, or specialist

- Clear member guidelines that outline what is and isn’t shareable

- A community-minded approach—not a for-profit insurance corporation

Some health shares even include:

- Telemedicine or virtual urgent care

- Discounts on labs, prescriptions, and imaging services

- Optional wellness plans or sharing for preventive screenings

Why Health Shares Are a Smart Fit for the Self-Employed

Self-employed individuals often value:

- Freedom of choice in healthcare providers

- Lower monthly costs that help stabilize unpredictable income

- Simple, transparent guidelines instead of red tape

- Direct, personal support when medical needs arise

Health share memberships align perfectly with that mindset.

You might be a great fit if you:

- Are self-employed

- Are under 65

- Are generally healthy with no serious pre-existing conditions

- Want a budget-friendly way to handle large medical expenses

One of the biggest reasons health shares appeal to self-employed individuals is the control they offer. You’re not stuck navigating a corporate bureaucracy—many members say the process feels more personal, straightforward, and even human.

Real-Life Member Experiences

Here’s what real Zion HealthShare members are saying:

“I cannot say enough good things about Zion HealthShare! I had an emergency room visit that turned into an overnight stay at a hospital after an emergency gall bladder removal last year. I have primary insurance but they did not help with the visit. I have Zion HealthShare as a backup. Zion HealthShare picked up the entire bill! I have to thank everyone there for all their hard work on this and for answering my prayers! Special thanks to Sabrina who is always kind and caring on the phone with me.”

— Mark B., Zion HealthShare Google Review

“My family and I have been members of Zion for only about 15 months now. Our experience through a catastrophic health emergency has been nothing short of fantastic. Not only does the team speak with care and compassion—compared to my hospital who tried scare tactics with me—but they genuinely come through with helpful suggestions, processing requests on time, and generally make for a great member experience. Rachel B. has helped give us tremendous peace of mind and coordinated all our shareable requests. She’s been responsive, polite, and effective. We highly recommend Zion if you are self-employed or a business owner. They will not disappoint.”

— Phillip K., Zion HealthShare Google Review

How Much Can You Save?

In 2025, the average monthly premium for a family of four on a mid-tier ACA insurance plan is approximately $1,650. That adds up to nearly $20,000 per year—and that’s before you’ve even used any healthcare services.

On top of that, the average family deductible is now over $8,400, meaning you could be out-of-pocket for nearly $28,000 before your insurance plan begins to help in a meaningful way.

In contrast, a health share membership for a family of four typically costs $500–$700/month—or about $6,000 to $8,400 per year. Most health shares also have a much simpler structure for medical needs, such as an Initial Unshareable Amount (IUA) of $1,000–$2,500 per need, depending on the plan.

That’s why so many self-employed families are making the switch:

- Lower monthly costs

- Simpler guidelines

- Freedom to choose your own providers

- And substantial yearly savings—often over $15,000 per year compared to traditional insurance

Instead of navigating billing departments and pre-approvals, you submit your bills and follow the health share’s process—often with direct reimbursement or bill negotiation support.

What Health Shares Don’t Handle

It’s important to know what health shares typically do not assist with:

- Routine prescriptions (though many offer discount programs)

- Preventive services (depending on health share or membership type)

- Small, everyday expenses that fall below your sharing threshold (IUA or MRA)

- Guaranteed payments (they are not insurance, though many are reliable and consistent)

They’re best for larger, unexpected medical needs—the kind that would otherwise leave you with massive bills.

Health Shares Aren’t for Everyone

If you need frequent medical care, costly prescriptions, or want everything bundled into one plan, a health share may not meet your expectations.

But if you’re self-employed, relatively healthy, and tired of overpaying for traditional insurance, a health share might be the best-kept secret in affordable healthcare.

Ready to Explore Your Options?

If you’re self-employed and ready to stop overpaying for traditional insurance, you don’t have to go it alone.

? Download our free guide: The Health Share Guide and Essential Checklist

? Check out our top recommendations: Best Health Share Plans (And Why Zion HealthShare Is My Top Pick)

Health shares are not insurance and do not offer insurance coverage. Membership in a health share does not guarantee the payment or reimbursement of medical expenses. Each organization operates under its own membership guidelines, which determine what expenses may be eligible for sharing. This publication is for informational purposes only and is not provided by an insurance company. For state-specific notices and full program details, please visit the respective health share’s official website.

vs Zion HealthShare")

Leave a Reply